About Long Term Care at Home

Book (2014): How to Deal with 21 Critical Issues Facing Aging Seniors

Book (2014): How to Deal with 21 Critical Issues Facing Aging Seniors

Aging seniors and their families are often confounded by the complexity of issues facing the elderly (including declining income, increased debt, poor investment returns, declining health, medical crises, complex insurance programs, long term care challenges, etc...). This book (published in 2014) takes a comprehensive approach to address these challenges and provide solutions.

$44.00 | $33.00 | 310 pages | Learn More...

by the NCPC

Care Provided By Family or Others at Home

Traditional Arrangement

Care in the home provided by a spouse or a child is the most common form of long-term care in this country. About 73% of all long term care is provided in the home environment typically by caregivers who receive no compensation for their labor.

The supervision of care or hands-on care from informal caregivers is limited to activities that don't require a skilled background. Lifting , bathing, dressing, diapering, toileting and helping with walking can be a challenge to family caregivers because they don't have the proper tools or are not trained in this area. Or the children of elderly care-recipients may have difficulty dealing with cleaning messy bottoms or bathing their parents. Another problem may be handling errant behavior from dementia or depression.

Because of this, some caregivers bring in paid providers to help with lifting, walking, bathing, incontinence, toileting, dressing and supervision.

Another home care arrangement is for family members, who are not living close by or who are employed fulltime, to become supervisors and coordinators of care and to offer only limited, personal, hands-on care. These people may hire a care manager to act on their behalf.

Home care is almost always provided in the home of the recipient or the home of a family member or friend. Home care may under certain circumstances be offered in other settings such as group homes or independent retirement communities. Below are some of the activities provided by or supervised by family caregivers.

- Help with walking, lifting and bathing

- Help with using the bathroom and with incontinence

- Providing pain management

- Preventing unsafe behavior and preventing wandering

- Providing comfort and assurance or arranging for professional counseling

- Feeding

- Answering the phone

- Making arrangements for therapy, meeting medical needs and doctors' appointments

- Providing meals

- Maintaining the household

- Shopping and running errands

- Providing transportation

- Administering medications

- Managing money and paying bills

- Doing the laundry

- Attending to personal hygiene and personal grooming

- Writing letters or notes

- Making repairs to the home, maintaining a yard and removing snow

Communal Arrangements

Informal Arrangements

In large urban areas where families have lived together in an apartment complex and grown old together, there is a possibility for residents in the complex to band together and watch out for each other. This might also include limited caregiving services for neighbors. But it more likely would include helping neighbors with such things as light housekeeping, shopping, companionship, medication reminders and transportation.

Another arrangement becoming popular in Europe is for the elderly to share an apartment or home together and provide for each other's needs. In Europe there are actually agencies that bring together interested elderly parties who desire to share living arrangements. We're not aware of these services in the United States , but the trend will probably be to provide the same living arrangements here. There are currently all kinds of agencies providing roommate sharing service around the country so it is only a matter of time before some of these services start specializing in bringing together elderly people who can provide support for each other.

Currently the only way we are aware of elderly people coming together to share a home or apartment is through classified ads. A daily reading of the newspaper or online ads will probably yield a number of offers from people desiring a roommate who can also provide some care services for each other.

Formalized Communal Arrangements--Shared Living Residence

A shared living residence provides private rooms and shared kitchen and living areas in a family home environment for 3 to 10 older people who share rental expenses and homemaking activities.

A shared living residence may be owned or sponsored by a community organization and rented to residents. Additional supportive and household assistance for residents will vary according to the independence level of the residents. No government licensure or certification is required unless personal care is charged for or provided by the sponsoring organization. Charges or rents may be priced at market rates or subsidized with government assistance.

Source: 1999 National Long-Term Care Survey

Source of the first two tables below is 1999 National Long-Term Care Survey

Source: 2005 Statistical Abstract Of The United States , Health And Nutrition

LENGTH-OF-STAY:

Because it is not typically covered by the government, inclusive statistics for how long home care can last are lacking. The 1999 national long-term care survey did ask how long caregivers have been offering care. We do not have the data for length of stay for particular types of conditions but reports from the survey indicate home care can last 3 to 5 years. The National Health Statistics reported that in 2007, services commonly used by home health care patients age 65 years and older include skilled nursing services (84%), physical therapy (40%), assistance with activities of daily living (ADLs) (37%), homemaker services (17%), occupational therapy (14%), wound care (14%), and dietary counseling (14%).

COST:

There is usually little ongoing cost for services with this type of care since services are mostly furnished free of charge by informal caregivers. However, there is a growing trend for out-of-state or fulltime employed caregivers to bring in paid provider services for home care. There can also be significant costs for supplies, medications, hospital equipment and home modification.

Supplies could include diapers, wipes, pads and personal hygiene supplies. These are paid typically out-of-pocket and surprisingly could cost as much as $200.00 to $400.00 a month.

Medications are currently not covered by Medicare and must be covered by the care-recipients, although Medicare prescription drug coverage is coming next year. Currently drugs could be costing an older individual $300.00 to $600.00 a month. Those requiring long term care are probably taking more medications than their peers in the community who are relatively more healthy.

Hospital equipment includes such things as special air beds, walkers, wheelchairs, scooters, stools, oxygen equipment, crutches and hospital beds. Generally these costs are covered by Medicare but co-pay must be made unless the recipient has a Medicare supplement policy which should pick up the additional cost.

Home modification could include building ramps, widening doorways, installing special showers and toilets, installing lifts and handrails. These costs are borne by the care-recipient or her family.

If the family finds it necessary to bring in a homecare agency to help with lifting, bathing, walking, incontinence, toileting, dressing or supervision the cost could be anywhere from $12.00 to $25.00 an hour depending on the area of the country and whether there is a contract for extended weekly services.

WHO PAYS?

As a general rule government programs will not pay for long-term care unless there is a medical need. The charts above demonstrate that the predominance of care provided in the home is non-medical and therefore government programs will not pay.

Government programs will pay for home care that is non-medical under certain conditions. The care-recipient must be low income and have virtually no assets.

As has been mentioned, this care is typically provided free of charge by informal caregivers who are family or friends. But increasingly, Medicaid is also paying for these home services for those who are Medicaid qualified. In order to receive Medicaid home care a person must qualify for Medicaid and spend at least 90 days in a nursing home. Medicaid qualification requires an income insufficient to pay for care and assets less than $2,000.00.

Local area agencies on aging sometimes in conjunction with Medicaid will often pay for home repairs, transportation and snow removal for low income recipients. In addition, many low-income people can receive rent subsidies and help with utility bills from Federal and local governments. The local area agency on aging can furnish information on these programs.

Medicare will also pay for home care services on a limited basis to help a person who is homebound recover from an injury or medical condition. Medicare provides a home health agency about 60 days worth of payment to help with the recovery. If the recipient fails to respond, deteriorates or is not improving in any way Medicare will no longer cover the cost of care.

For people with low incomes, area agencies on aging provide some free help. There are volunteers who will sit with a care-recipient to give some free time to the caregiver. There is meals on wheels at no cost or very low cost. Senior centers are usually sponsored by area agencies on aging and they sometimes provide transportation for a disabled person at home. If the person requires no medical attention, the caregiver can allow her care-recipient to spend some time at a senior center and she can get some rest. About three years ago Congress appropriated some money for caregiver respite. This should be available to all caregivers regardless of income level. Area agencies also provide legal help, counseling, caregiver support groups and a whole raft of other benefits. And of course the local agency is a great resource for other senior support programs that are available in the area. Click here to find a list of area agencies on aging.

For those who had the foresight to buy long-term care insurance, the insurance will cover the cost of home care either for help with activities of daily living, with supervision for dementia and, if it is a newer policy, for help with many of the other activities listed at the beginning of this section. These activities are called "homemaker services". Most policies will pay in addition, for home modification and other necessary training and support to help a person remain in the home.

A recent survey by LifePlans, Inc. (see table below) indicates that people with insurance will purchase services they normally would have furnished for free themselves. This is an extremely important issue because caregivers may often have money to pay for these services but will not spend it because, as they reason, they may need the money after their loved one is gone. By not seeking help, many caregivers destroy their own emotional and physical health struggling to provide countless hours of care for a loved one. The insurance survey specifically pinpointed the fact that with insurance to help, the stress from caregiving was substantially reduced, especially for caregivers who were employed and working outside of the home. Caregivers were given a needed rest. And unlike the tendency to avoid using personal funds, people with insurance will almost always use it and make claims to help with care.

The Veteran's Administration will also pay for home care for qualifying veterans on a basis similar to Medicare: however, it is probably paid more liberally without a definite cut off of services. Under VA rules as with Medicare there must be a medical need for care in the home. VA home care must be approved by a medical staff at the local veteran's hospital.

Source: LifePlans, Inc

Paid Providers of Long-Term Care in the Home

Home Health Agency Care

DESCRIPTION:

In 2010, about 33,000 home health agencies served approximately 12,000,000 clients across the United States. Annual expenditures for home health care tin 2010 were projected to be $72.2 billion (source: Centers for Medicare & Medicaid Services, Office of the Actuary). In that year Medicare spending accounted for approximately 41 percent of home health expenditures. Although current figures are not yet available for 2014, the number of home health agencies has been going up year after year as well as the number of clients being served.

In the United States, the rate of home health care use for women aged 65 and over was 55% higher than the rate for men. Female home health care patients aged 65 years and over were more likely than male patients to be 85 years and over and were almost three times as likely to be widowed (SOURCE: National Health Statistics Reports 2012).

Although home health agencies are privately owned, Medicare is the principle payer for their services. Home health services through Medicare are available under parts A and B. In order to qualify for Medicare homecare a person must have a skilled need, must be homebound and there must be a plan of care ordered by a Physician. Prior to 1997 Medicare typically paid for home care for as long as it was needed. Prior to 1997 annual Medicare costs were almost double the amount cited above. In order to save money Medicare has since gone to a prospective payment system where, according to the plan of care, a certain amount of money is allocated to resolve the skilled need for the patient. Monies are typically provided for a period of up to 60 days. If the patient recovers sooner then money may have to be reshuffled to other patients who are not responding as well. At the point where the patient does not respond or improve, no more Medicare money is forthcoming. After Medicare cuts off, a person continuing to need long-term care services must find sources other than Medicare.

Home health agencies deliver a variety of skilled services outlined by the chart below. The plan of care always includes as well custodial services to help the care-recipient remain in the home. These would include an aide for an hour or two a day to help with bathing, dressing and transferring. If there is time remaining other personal services may be offered as well. These personal services are also covered by Medicare.

Recently Medicare has redefined what it means by "homebound" to allow recipients to leave the home on a limited basis. Beginning in 2003 and ending three years later, Medicare is testing, with a very small test group, a program where selected home health agencies can provide adult day health care instead of home health services. If successful the program will offer a new dimension in Medicare home care. In addition, under the new definition, Medicare will also allow and pay for home visits from doctors who specialize in homebound elderly patients. Limited office visits are also allowed under the new definition. Finally, in the past few years Medicare is paying for home telehealth visits through a home telehealth, computer work station. Telehealth is being used with some success to provide home care in rural areas where it would be difficult to arrange the personal visit from a home health care agency. To learn more about Telehomecare click here.

Source: 2005 Statistical Abstract Of The United States , Health And Nutrition

Source: 2005 Statistical Abstract Of The United States , Health And Nutrition

Source: 2005 Statistical Abstract Of The United States , Health And Nutrition

LENGTH-OF-STAY:

Although Medicare- will authorize up to 60 days at a time of home care, according to the Centers For Medicare And Medicaid Services (CMS) the average length of stay for Medicare home care services is 41.5 days. Oftentimes a person continues to need supervision or care after Medicare quits paying but the payment for that will have to come from someone other than Medicare.

The number of home care patients as a percent of all individuals in that age group goes up drastically with age. Even though the age group of 85 and above represents only 4% of all the aged population it accounts for about 28% of all patients. The bulk of the aged population is between the ages of 65 to 75 but only accounts for about 27% of all home care patients. Total patients for the aged over age 75 account for the other 73%.

A common statement from individuals who are confronted with the need for long-term care planning is,

"I'm in good health, I'm going to live a long time and I won't need long-term care."

The statistics show otherwise. In fact it is estimated that about half of the population over age 85 is receiving long-term care.

COST:

Since about 90% of all home health agency care is paid for by Medicare or Medicaid, the cost of care is not necessarily relevant for this study. But some families do pay for this service out of their own pockets. Costs will vary from area to area. A nurse, therapist or social worker may cost $70.00 to $100.00 an hour. An aide to take care of daily living needs, so called activities of daily living, may cost $10.00 to $25.00 an hour.

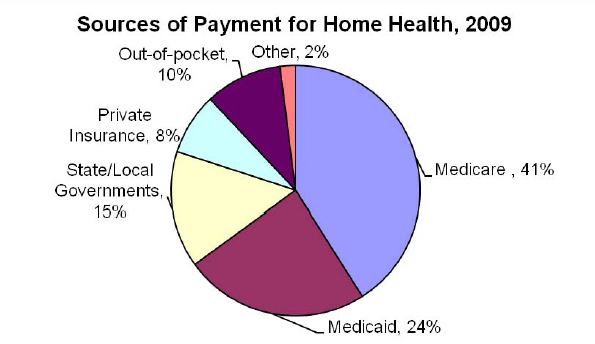

WHO PAYS?

The chart below shows that Medicare and Medicaid pay 90% of the cost of home health agencies services. The other 10% is shared by families, and private insurance. As more people buy long-term care insurance, they will also be more prone to utilize the services of home health agencies. However, this is only after Medicare has paid its portion. This is because all long-term care insurance policies will only pay after Medicare has paid its obligation.

A new trend for home health care is for agencies to furnish care through a cadre of non skilled employees for families who do not qualify for Medicare or Medicaid homecare but still need help with loved ones at home. The future trend will be for more and more of the cost of home care services to be paid by the family or by insurance if it is available.

Source: 2009 Centers for Medicare and Medicaid Services, cms.gov

Live-In or Privately Hired Caregiver

DESCRIPTION:

Live-In or Privately Hired Caregivers. Sometimes a spouse or child wants their loved one to remain at home as long as possible. But the need for care is overwhelming to the family or the spouse and they simply can't provide it on their own. If funds are available, the least expensive way to solve this problem is to hire directly someone who is willing to come into the home for extended periods of time and provide that care. This arrangement is more typically used in the case where care or supervision is required on a 24 hour basis. These providers would typically not have medical skills. If medical care were needed a nurse or therapist would also be hired from a home health agency.

For a live-in caregiver the opportunity to have a place to live is partial or perhaps complete compensation for providing that care. If there is extra room in the home of the care-recipient this is an ideal arrangement. Or even without a living arrangement, a family hiring a caregiver not living with the care-recipient, could spend considerably less than paying the cost of an aide from a home health agency.

Married college students who have small children might be a likely source for caregivers since they would typically have low income and housing would be a priority need. A live-in arrangement would provide the housing in return for care and possibly some additional income for the young couple. Oftentimes a grandchild is looking for a place to live and is willing to provide this care in exchange for room and board. Or the grandchild may be compensated by the family in addition to the room and board. Also a single woman with inadequate income and living in an area where housing is expensive might be willing to agree to a live-in care arrangement. Finally, some older individuals are looking for the opportunity to nurture and care for other elderly individuals or couples. These benevolent people are willing to come into the home and provide care in return for a moderate compensation to cover their time and costs.

We're not aware of agencies that facilitate these arrangements. A private caregiver would have to be acquired through advertising. This might include posting notices near a college campus, in a senior center or advertising in the newspaper. The section on care managers also includes a description of care managers finding a personal care provider for a fee.

A major disadvantage of hiring somebody privately is ensuring this new employee is trustworthy and will provide the care needed. If possible, arrangements should be made to make sure the new caregiver is bonded to protect the family from theft. But what if the caregiver turns out to be unreliable, lazy or abusive? Elder abuse is very prevalent in this country and estimates are that 10% of the elderly population is being abused by family or caregivers. If a private caregiver is hired great care should be taken to investigate that person's background and history of employment.

LENGTH-OF-STAY:

The advantage of a private care arrangement is that help can be found to allow a care-recipient to remain in the home for as long as possible. In fact, as a person deteriorates and requires more medical attention, if there is money to pay for doctor's visits and nurses, a person need never enter a facility to receive long-term care. Ideally that person could die in the home surrounded by loved ones in an atmosphere more supportive of a positive end-of-life experience.

COST:

Many individuals are willing to provide this care based on a weekly or monthly salary or contract arrangement which could be the equivalent of $5.00 to $8.00 an hour. This would be much more affordable than the hourly rate from a home health company of $10.00 to $25.00 per hour. Or the care could be virtually free if the live in care provider were willing to accept only room and board in exchange for the care. Remember though that this is compensation in-kind and must be reported to the IRS.

WHO PAYS?

This care could be provided by two paying sources. One might be long-term care insurance. Most policies require that someone providing care in the home has to come from a licensed agency. There are a few policies that will allow care in the home to be provided by anyone the company approves. It would make sense though, the insurance company would not just approve anyone but the care provider would have to have experience, probably have to be licensed and most certainly be bonded.

The other most likely source of payment would be from the care-recipient's income or assets or the family of the care-recipient may be willing to pay for this kind of care.

Regardless of who pays, the care provider will be considered an employee by the IRS. As such, income tax, Social Security and other payroll taxes must be withheld by whomever is paying the bill. We're all well aware of media focus on candidates for public office who have hired individuals to watch over their children or to be housekeepers but have failed to pay necessary payroll taxes to the IRS. There are stiff penalties and fines associated with hiring someone and not paying the taxes.

There is no possible way to arrange a private payment hiring agreement for someone to come in the home and for that person not to be considered an employee. The method of payment--hourly, piecework or contracted--is irrelevant to the IRS. What is important to the IRS is whether the employer has control over the employment hours of the person who is hired. Since this would always be the case with privately hired care providers, the IRS could care less how the person is compensated. Payroll taxes must be paid. On the other hand, contracting this service from a company that provides it, is not an employer/employee relationship and does not require payment of payroll taxes.

If you do hire someone to provide care in the home the IRS has a publication to walk you through the tax reporting and withholding process. It can be found on the following URL: https://www.irs.gov/pub/irs-pdf/i1040sh.pdf

Personal Care or Non-medical Home Health Care

DESCRIPTION:

Non-Medical Care Services In The Home. These providers represent a rapidly growing trend to allow people needing help with long term care to remain in their home or in the community instead of going to a care facility. The services offered may include:

- companionship

- grooming and dressing

- recreational activities

- incontinent care

- handyman services

- teeth brushing

- medication reminders

- bathing or showering

- light housekeeping

- meal preparation

- respite for family caregivers

- errands and shopping

- reading email or letters

- overseeing home deliveries

- dealing with vendors

- transportation services

- changing linens

- laundry and ironing

- organizing closets

- care of house plants

- 24-hour emergency response

- family counseling

- phone call checks

- and much more...

A search of your local Yellow Pages under "home health agencies" will reveal that a large number of the advertised providers are personal care or non-medical home health companies. This causes some confusion since the yellow pages choose the same classification to list non-medical and traditional home health agencies together.

Personal care agencies are different from traditional home health agencies in that they do not provide medical services or skilled services and they are not paid by Medicare.

In addition, many states do not require personal care agencies to license with the state health department. In some states a person desiring to start a business like this need only advertise, get a business license and start hiring employees. On the other hand, some states require these companies to meet the same stringent rules under which traditional home health agencies operate. This might include hiring trained employees, the use of care plans, periodic inspections by the state health department and bonding.

If you live in a state which does not require regulation of these companies, it is important for you to check the background and history of these providers before using their services. Another benefit for the public is that many of these companies are part of a national franchise system. There are a number of these home care provider franchises around the country. Being a franchise, it is more likely that you can trust the services of the company and not have to worry about theft or abuse with your loved one.

Many larger traditional home health agencies are integrating non-medical services into their care delivery. This means Medicare and Medicaid are not paying the bill for this portion of a home health agency's business. Also many large integrated facilities providers (combined nursing homes, assisted living and independent retirement arrangements) are offering more non-medical or personal home healthcare.

The number of these companies is literally mushrooming all over the country. It is evident from this growth that there is a growing need for traditional family caregivers to contract help from paid care providers. This is probably due to the fact that many of the traditional caregivers are now employed fulltime or are living a long distance away from their loved ones and find it difficult if not impossible to provide long-term care.

Home Repair And Maintenance Services. As a general rule most personal care agencies provide only aides to help with personal needs in the home. Very few offer such things as deep housecleaning, home repairs, remodeling or yard maintenance. There is now a growing trend for companies to specialize in providing these additional services for the elderly. And as with personal care agencies many of these belong to national franchises.

It is evident that there is a growing national need to provide services to allow people to remain in their homes as long as possible. The growth of companies providing these services is evidence that this is a preference for the elderly needing care in the community.

Monitoring Services. These are companies that provide GPS based bracelets or pendants to track the elderly at home who tend to wander. Or the companies may provide alarm devices such as pendants or bracelets which allow the elderly to alert someone if there has been a fall or a sudden health-related attack. In the event of an alarm, a 24 hour monitoring service will alert the family or medical emergency services. In addition there are companies that will install video cameras in the home to monitor the elderly on a 24 hour basis.

Finally, there are companies that will check in with the elderly on the telephone from time to time to make sure that they are all right. The service may also include medication reminders and prompting for the elderly person to make sure meals are prepared and unsafe behavior is avoided.

LENGTH-OF-STAY:

As has been mentioned earlier in this paper homecare can last anywhere from three to five years . The big question is whether home care is always appropriate. Oftentimes the care-recipient will want to stay in the home when other care environments are more appropriate. The use of paid home care services definitely makes it an easier decision to remain in the home but the cost could far outweigh the cost of other services such as an assistant living facility or allowing Medicaid to pay for a nursing home.

COST:

Non-medical home services run about $10.00 per hour to $25.00 per hour depending on the area of the country. Many of these providers will offer lower rates if the family contracts for certain levels of care. This is based on the hours weekly or monthly provided by the company. The more hours provided the less the cost per hour.

Generally in rural areas the cost of personal care would be less than an urban areas. In urban areas with high cost of living such as cities in the Northeast expect the cost to be higher than in urban areas in the South or the Midwest .

WHO PAYS?

The cost of this care is primarily paid by the family. But non-medical care can also be subcontracted through Medicare paid home health agencies or through Medicaid waiver programs. In this case the cost would be covered by those government programs. Hospice services which are covered by Medicare as well may also subcontract with personal home care services. Local government programs may also have funds to provide home maintenance services for the elderly poor. This might also include snow removal and transportation services.

Long-term care insurance will also pay for these services. The catch is that the care provider must be state licensed in order for the policy to pay. In those states where care providers are not licensed this could be a problem. Although there is a growing tendency for traditional home health agencies to provide this care and they are always licensed.