Paying the Cost of Care

by the NCPC

Planning for Out-Of-Pocket Costs

Determining The Cost of Long Term Care

The Effect of Inflation

Funding Options

Planning for Out-Of-Pocket Costs

Understanding the Need for Formal Care or Informal Care

As we learned in previous sections, informal caregivers are family members or friends who take care of loved ones typically without being reimbursed for their services. Formal caregivers are paid professionals or volunteers from aging organizations. Whether they are reimbursed for their services or not, formal caregivers receive some sort of funding either as wages or salary or for administration of their support group.

The chart below illustrates the relationship of informal care to formal care. As care needs increase, both in the number of hours required and in the number or intensity of activities requiring help, there is a greater need for the services of formal caregivers. Unfortunately, many informal caregivers become so focused on their task they don't realize they are getting in over their heads and they have reached the point where some or complete formal caregiving is necessary. Or the informal caregiver may recognize the need for paid, professional help but does not know where to get the money to pay for it.

It is the job of a care manager or a financial adviser or an attorney to recognize this need with the client caregiver and provide the necessary counsel to protect the caregiver from overload. The advisor can also likely find a source for paying for formal care that the caregiver may not be aware of.

Intermittent Care

This would require the occasional attention of an informal caregiver but there may also be a medical condition that may require expertise the informal caregiver does not possess. As a general rule most people receiving this kind of care would probably be in their own home and the caregiver would be living or working close by and stop only for occasional visits.

There is, however, a growing trend where the only family caregivers may be living hundreds or thousands of miles away from their loved one. In this case, a care manager would be hired to arrange for the intermittent care for the loved one.

Part Time Care

This could still be furnished by an informal caregiver assuming there is no extensive medical condition requiring frequent attention. It is more likely under this scenario the care-recipient and the informal caregiver would be living together. Or with no caregiver available a decision would have to be made whether it would be in the best interest of the care-recipient to receive formal care in the home or to go to a care facility. Oftentimes a care facility can offer a better environment at a lesser cost. On the other hand, many care-recipients prefer to remain in their homes at all costs. And for long distance caregivers, hiring a care manager is still the best option.

Full-Time Care

Full-time care can often be offered by informal caregivers living with the care-recipient. But this arrangement is not always in the interest of the caregiver. Because of the demand on a caregiver's time and attention, this arrangement will often result in the caregiver suffering from severe depression, social isolation and the development of medical ailments. Again, the decision is often dictated by the lack of funds to pay for professional care. But when the need for care has progressed to a fulltime basis, advisers or family should be looking to implement formal care delivery either in the home or in a facility. As with the other care options above, a care manager could prove invaluable in selecting the setting and the care providers.

Depending on what causes the need for long-term care, a care-recipient could start out at any point on the curve. For instance a stroke, injury or sudden illness may result in the immediate need for part time or fulltime care. On the other hand the slowly progressing infirmity of old age, the slow onset of dementia or a progressively deteriorating medical condition may only require occasional help; beginning with intermittent care from an informal caregiver but gradually progressing to the need for fulltime, formal care.

The Longer the Need for Care the More Likely the Need for Formal Care

The care progression curve above also illustrates an important principle with long-term care. It takes time for the need for formal care to manifest itself. Short duration, long-term care situations can often be handled by health insurance or Medicare service providers. In addition, families may have the resources and the stamina to get through short periods of care without paying for help. As the days turn into months, the care recipient typically worsens and requires more attention and the ability of informal caregivers weakens. Long duration care situations almost always result in the need for bringing in paid, formal caregivers or for placement in a facility.

Although the need for long-term care will happen to about one out of two of us, that need may not be longer than a few weeks for a few months. But none of us know whether our need for care will be of long duration or short duration and it is important when planning for long-term care to plan for the worst-case scenario.

Wealth Characteristics of Elder Households

The two charts below illustrate the relationship of pre-retirement income to post retirement income. Notice that prior to age 65, about 60% of all households in the age group of 55 to 64 earn $50,000 or more a year. These years are usually considered the highest earning years. Note that at age 65 and older this earnings group has dropped in half to about 33% of all households. Also note that prior to retirement only about 26% of households earn less than $35,000 a year. But after age 65, this demographic group has doubled to about 50% of all households. This is just an illustration of what everyone already knows, that income goes down after retirement.

Knowing that their income will be lower, many elderly rely on retirement savings and investments as well as the equity in their home to provide additional income when needed. It's surprising the high level of asset ownership for America 's elderly generation. Note from the chart below that well over 70% of those over 65 own a home, own a savings account and own one or more vehicles

source: statistical abstract of the United States, 2006

source: statistical abstract of the United States, 2006

Classifying Household Wealth Groups

We believe the preceding charts illustrate a natural selection of elderly households into three distinct groups. We will call these

- Low wealth households,

- moderate wealth households and

- high wealth households.

Low Wealth Households -- It appears a natural income division occurs around $25,000 to $30,000 or less of income a year. We will call this group the low wealth household group. Our rough estimate is this represents about 40% of all households with members over age 65. Based on our experience in dealing with folks in this age group, we find that a number of them may own a home, but not one of high-value. A number making less than $14,000 a year may also be renting or relying on government housing assistance. Some in this group may have retirement savings but probably not more than $10,000 to $20,000 total. And they consider this to be money that should only be spent in an emergency or when things get really tough.

Moderate Wealth Households -- The next natural division appears to occur in an income range from $$30,000 a year to around $70,000 a year. We think this might represent about 45% of elderly households. In our experience, a single person earning $35,000 a year, with no debts and moderate savings and investments can probably live comfortably in retirement. Of course this depends on the cost of living in the area and assumes there are no house payments. It would probably take about $40,000 to $45,000 a year to provide the same standard of living for a couple. Those elderly people in this range, either single or married, probably own a home with a reasonable equity value and they probably have retirement savings and investments in the range of $20,000-$100, 000.

High wealth Households -- This group represents those who planned well for retirement. These people, whether single or more likely married, probably represent about 15% of elderly households and would have incomes of $70,000 a year or more. They would most likely own one or more high-value homes and probably have no less than $100,000 in savings and investments but more likely have $200,000 to $500,000 in additional assets.

We also want to point out that our classification of wealth groups is not based on rigorous research but on a loose interpretation of the data above as well as our own experience in providing advice to these groups of people. The main purpose for identifying different wealth levels is to help our readers understand which groups are more likely to pay the cost of long-term care entirely out of pocket. We also adjusted our percentage of these age groups based on the fact that many folks age 65 to 70 are still working and their incomes would distort the numbers in the charts above.

The Likelihood of Paying Out-of-Pocket Based on Household Wealth

The chart below is not based on any hard research but is an attempt to illustrate the obligation of the three household wealth groups above in covering the cost of long-term care.

We have already pointed out that initially most long-term care is provided free of charge by family members or friends or volunteers. Typically the need for more intensive care evolves over time and this produces the need for paid, formal caregivers. But who pays for this care is directly related to the financial circumstances of the person needing care.

Based on our experience, the low wealth and moderate wealth households are going to rely more on non-paid family members to provide the bulk of initial care. This represents the dark blue area in all three bars below. High wealth households are more prone to hiring help instead of relying on family. The dark red area represents the fact that Medicare will provide the same amount of limited services to all three household categories regardless of income or assets. The light yellow area is the one that merits our attention. This is the focus of this entire section. How much of a family's income and assets must be spent to provide care when the family can no longer provide free care?

We believe the answer to this depends on the household wealth category of the person needing care.

A low wealth household is going to run out of assets quickly. There is a possibility of using the house and a reverse mortgage to pay for care at home, but our experience with people in this category is the family is eager to try and keep the house and instead have Medicaid pay for the care. Whether that can be done or not in an era of tightening budgets is questionable but it keeps the elder law attorneys busy trying to find a solution. Medicaid is hardly ever be desired solution but it is typically the only alternative. Long-term care services can cost anywhere from $2,000 to $6,000 a month. Care recipients who don't have the income to cover this will be subsidized by Medicaid after spending all assets down to $2,000 or less. The problem with Medicaid is most people would prefer to stay in their homes or even in an assisted living facility but in the majority of cases Medicaid will put them in a nursing home. Low income and few assets simply mean a care recipient has lost any choice in the care setting he or she may want.

People in the moderate wealth category are typically going to be able to stay in their home longer. They will have the means to pay for aides or possibly a privately hired, live-in caregiver. If they choose not to remain in the home, they have the option of a nice assisted living facility in a pleasant, home like environment. For these people it may be years before the assets run out and Medicaid becomes the only choice. Care recipients with moderate wealth have more choices in their care settings.

High wealth households have a peculiar dilemma. They typically have enough income and/or assets to maintain themselves in the home as long as they want. But the reason they have high wealth is because they prepared themselves for retirement and have deliberately provided adequate income and assets. These resources were set aside to enjoy their retirement years or to provide security for a spouse. It is possible the cost of long-term care could rob them of these dreams. Oftentimes, a healthy spouse caregiver will labor to provide care and destroy his or her health trying to avoid a spend down of these precious assets. It is this age group that should be the most concerned about providing future funds specifically for long-term care services. And ironically it is often this group that fails to do any long-term care planning in pre-retirement years because the anticipated availability of income and assets lulls them into a false security. Their typical response to a challenge to take up planning is should the need arise they will have plenty of money to cover it.

Pre-Retirement Planning for Paying the Cost of Care

Options to pay the cost of long-term care during retirement should be initiated when someone is in his 40s or 50s and not after retirement. If money is being set aside, this must be done early enough to provide adequate funding levels. If the intent is to buy long-term care insurance, waiting until retirement may be too late.

The cost of new policies is going up about 10% a year. And whereas a few years ago, a person in his late 60s or early 70s could qualify medically for a long-term care policy, ever tighter underwriting rules are resulting in a large number of denials for coverage. And then there's the problem of the premiums. Retired people, on a fixed income, may find it difficult to pay the high cost of long-term care insurance. But for those who waited and did not act in earlier years, there is the possibility of using a reverse mortgage to finance the cost of long-term care insurance. We will discuss this further on.

Determining The Cost of Long Term Care

In order to plan financial for your long term care, you need to know what the costs are now and what they will be in the future.

Current Costs

Every year Metlife conducts a national survey of nursing home and home health agency costs. This is a valuable resource for determining the cost of care in your area. Included below is the August 2003 survey. You can obtain this survey online by going to:

MetLife Survey of Nursing Home, Assisted Living, Adult Day Services & Home Care Costs

How Reliable Are National Cost Surveys?

Nursing Home Phone Sample, Cost Surveys

We recently completed a survey of the cost of all nursing home beds in our state. We then calculated the average cost and the median cost on a weight adjusted basis of the number of beds in a given cost category. Our average cost was significantly and statistically less than a national sample survey for our state in the same year. Our median cost (the halfway point cost of all beds more costly equal to the same number of beds less costly) was significantly less than our average cost and the national survey cost.

We believe that it is not possible to do a reliable sample phone survey of nursing home costs because all nursing homes in a given state are not the same in structure and operation and marketing philosophy. Because of a lack of uniformity, all nursing homes in the state will not follow a standard statistical distribution on costs and therefore a random sample survey will not give reliable results.

We could probably use up six or seven pages describing in detail the factors that affect private-pay bed rates for nursing homes. Also the application of these factors and different state approaches on regulating nursing homes affect the private-pay bed rates from state to state. Here are some of the factors:

- State regulation allowing skilled only or also intermediate care facilities

- The number of beds the nursing home has. Unless the survey results are weighted per bed, a 20 bed facility at $160 a day added on to a 100 bed facility at $120 a day and divided by two is going to make it appear that the average cost between those two facilities for a bed is $140 a day. But the real cost per bed between the two facilities is the weighted average. Which is $127 a day.

- The degree to which a state attempts to control the supply of beds and the subsequent occupancy rate

- The number of non-certified nursing homes that cater to the wealthy and charge higher rates

- The number of specialty nursing homes that use a different private pay long term care rate structure

- State Medicaid reimbursement procedure and policy which may affect the setting of private-pay rates

- State imposed staff ratios which may vary from state to state and vary for different types of facilities

- Whether Medicare reimbursement for a particular area is covering actual costs and if that is reflected in private-pay rates

- Whether an existing home has paid its plant costs or is still amortizing those costs

- The cost of liability insurance from region to region and state to state

Assisted Living Cost Surveys

Sample phone surveys for assisted living costs are acceptable as far as they go, but they probably don't reflect the entire assisted living service market. Surveys are not reliable as a comparison from state to state because of the differences in services offered between states.

The term "assisted living" is a marketing tool that refers to a large number of different community living arrangements that also offer care. There is no uniform regulation of these services from state to state. Some states regulate on the basis of number of residents while other states regulate on the basis of services offered. Not all states use the term assisted living for these living arrangements. In the states that control services, some of those states allow very little in the type of services offered and residents in those states must go to a nursing home to receive more extended services. On the other hand, some states allow assisted living to offer nursing home skilled services under certain conditions. Obviously the services offered will affect the cost of care and the cost of an assisted living arrangement. Also in some states assisted living cost includes the cost of long term care services and in other states the cost is charged in addition to room and board.

A large number of operations offering community living with care are invisible to the public. They are small operations that don't advertise and probably fail to register with their state health department. Their residents come to them via referrals from others. For purposes of classification we will call these "board and care " facilities.

These are operations using a residential home and housing residents in bedrooms in the home, sometimes shared with another person. Dining facilities, living room and bathrooms are shared. Some of these operations are employer and employee companies but the vast majority are run by the people who own the home and have taken in aged boarders to supplement their income. Long term care services are usually limited to what the owner operators can handle themselves. To augment services, a number of these operations will bring in home health agencies to help with medical conditions.

Board and care operations naturally have a lower cost of operation and will charge their residents typically much less than the apartment-based assisted living facilities included in national surveys. The surveys will not include these providers because they don't advertise, they don't list in the phone book and many have failed to license with their health department.

Home Health Agency Cost Surveys

Since 85% to 90% of home health agency cost is covered by government, such surveys are of little use to the public because the government will pay for it.

What would be very useful is if surveys were to include the cost of non-medical home health services. These costs are borne by the public and it would be useful for planning purposes to know what the cost is in a given area. Perhaps the national surveys will add this information in the future.

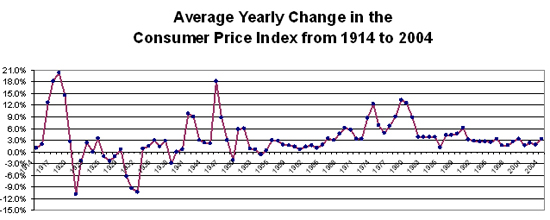

The Effect of Inflation

About inflation

Inflation is generally defined as in increase in prices for goods and services over a period of time. Persistent inflation seems to be an underlying phenomenon in the US economy. In fact economists and business consider an inflation rate in the neighborhood of 2% to 4% a year to be beneficial since it stimulates demand. The current government target seems to be around 3% a year. Knowing that prices will be higher in the future, consumers, both individuals and businesses, will not put off purchases very long. A continued level of purchases keeps the economy rolling. The chart below reflects this underlying inflation rate.

| 3.45% -- | 91 years from 1914 to 2005 | ||

| 3.96% -- | 55 years from 1950 to 2005 | ||

| 2.99% -- | 15 years from 1990 to 2005 | ||

Source: Bureau of Labor Statistics

Sometimes for various reasons, perhaps due to tight money supply or shortages or following a period of high inflation where purchasers have bought ahead and then decide to hold onto their money, prices for goods and services can fall rapidly in high levels of decline. This is called deflation and it can be very destructive. Deflation generally results in consumers deferring purchases and holding onto their money anticipating lower costs in the future. This can often result in a so-called deflationary spiral where lack of spending throws people out of work which leads to more lack of spending which leads to more unemployment. This leads to loan defaults and bank failures which further destroy the economy. The 10 year period of the Great Depression in this country is an example of this and were it not for the economic stimulus of the Second World War, that depression could have lasted even longer. Governments try to avoid deflation at all costs.

Very high inflation rates are also considered detrimental. This tends to punish certain participants in the economy such as those on fixed income or lenders and investors with long-term fixed interest loans or investments. And eventually high inflation, which is often tied to high demand, can result in a drop-off in demand when needs have been satisfied, shortages have discouraged buying or the market is saturated. This can then lead to a recession or even a depression.

Measuring inflation

Economists and the government use a number of tools to measure inflation but the tool most often used and most recognized by the public is the Consumer Price Index or CPI. The Consumer Price Index is considered the best measure of inflation for the day-to-day buying activities of the average American. The CPI is also used as an indexing tool to help pensions keep up with inflation, to provide cost-of-living increases to workers, to adjust levels of taxable income, to allow government benefits to match inflation and to make sure Social Security benefits do not fall behind.

The CPI is produced monthly by the Bureau of Labor Statistics, an agency in the Department of Labor. Every month over 80,000 different items and services are priced in selected urban areas and in selected locations. Prices are reported to the headquarters of the Bureau and adjustments are made to reflect changes in packaging and substitution of equivalent services or goods. Price changes are then applied to over 200 different categories in the CPI. This might include food items, energy, transportation, government fees, communication, health care, housing and so on. Price increases or decreases are calculated to reflect changes to a standard index that was established in the 36 month period from 1982 to 1984 and was set to equal 100. Indexes are easier to use to compare relative changes in prices. As an example a consumer Price Index in December of 2005 equal to 148 represents a 48% increase in the CPI since the base years.

The most commonly quoted percentage change from month-to-month or year-to-year is the change in the broad-based CPI which is called the Consumer Price Index for Urban Consumers.

But the BLS also tracks price changes in various categories such as energy or health care and so on. Not all prices change the same. It is well known that health-care costs go up much faster year-to-year than the broad-based CPI. And in some years energy costs may increase faster or slower. Economists and the government are also interested in the CPI component that reflects housing prices.

Managing inflation

Since the double-digit inflation of the late 1970s and early 1980s, the government has been very focused on maintaining a sustainable level of inflation. The responsibility for this task has fallen largely on the United States Federal Reserve Bank. The bank does this primarily by controlling the supply of money.

During periods of high inflation, there is a need for more money to pay the higher prices. Money may come in the form of higher wages or salaries or higher interest rates or from loans but in our modern economy additional physical cash is actually generated through credit or bank draft or stock margin transactions. Only a small percentage of purchases in this country are made with currency -- paper bills and coins. Purchases are made by using bank drafts, personal loans, collateral loans, equity loans, margin accounts, credit cards or through credit accounts with the sellers of goods and services.

The Federal Reserve Bank uses interest rates to control the supply of credit and to a great extent the supply of money. When it's difficult or costly to obtain more money for purchases, then demand falls and with it prices fall as well. But the Fed walks a very tight line. If it reduces demand too much, this can cause higher unemployment and possibly a recession. If it allows for too much money to flow into the system, this can stimulate inflation and cause problems as well.

The Federal Reserve Bank of the United States has the following responsibilities:

- It is the bank for the federal government and disperses funds for government purchases.

- It is responsible for buying and selling government securities such as bills and bonds on behalf of the US government.

- It distributes and maintains the supply of paper bills and coins in circulation.

- It regulates and provides banking services such as loans and check clearing for all private, federally chartered banks in the United States .

- It overseas operations of foreign banks in the United States and foreign operations of U.S. banks abroad.

- When called upon it can buy or sell other currencies in order to stabilize exchange rates.

It is the loan services that banks require from the Fed, that are the primary tool for controlling the money supply. Banks, daily, need to loan money to each other in order to maintain minimum levels of federal deposit reserve requirements. Banks charge each other interest on maintaining this loan reserve service and the Fed facilitates these loans. This inter-bank interest is called the federal funds rate. When the federal funds rate is high, this increases the cost of business to banks and they must pass it on to consumers in the form of higher loan interest rates. A low federal funds rate reduces loan interest rates.

It is the supply of excess money in the Federal Reserve system that determines the federal funds rate not the Fed itself. But by controlling this money supply the Fed can basically control the rate. This is done through so-called "open market transactions". If the Fed wants to lower the funds rate it will buy government securities. Those who sell government securities receive checks (or more typically direct credit deposits) from the Federal Reserve which will be deposited in federal reserve banks. This increases the supply of money in the Federal Reserve system and provides additional funds for overnight bank loans. This increase results in a lower interest rate. If the Fed wants to increase interest rates it will step up its domestic sales of government securities. Proceeds from the sale will be applied to an increase in government revenues and money will flow out of the banking system. In essence, a sale of government securities takes money from buyers and in turn from banks and removes that money from the economy.

Starting in the early 1980s, under the direction of Fed Chairmen William Volker and continuing with his successor Alan Greenspan, the Fed has used various economic predictors to try and guess the direction of inflation and apply primarily the policy outlined above to affect interest rates. It should be noted other strategies are used as well but open market transactions are the most commonly used method to control interest rates.

Prior to this period, the Fed was focused primarily on measurements of the money supply. Changes in the supply and resulting interest rates were maintained by an appropriate monetary policy. Unfortunately, over the years, an evolving sophistication of capital markets in the United States made these measures of money supply less relevant and techniques to modify the money supply in the late 1970s were not as effective in controlling inflation as they had been in the past.

Differing Rates of Inflation for Long-Term Care Services

When planning for long-term care it is important to know that inflation rates for various services are different. For example nursing homes have traditionally increased in cost year-to-year at a much higher rate than the broad CPI. We will examine the following six types of long-term care services and try to give you an idea of what to expect in future inflation rates.

- Nursing homes

- assisted living

- adult day care

- hospice

- home health agencies

- non-medical home health care

Nursing homes

The chart below is from data from the US Bureau of labor statistics for the consumer price index of urban nursing home costs and home health aide costs from 1978 to the present. Recently the BLS has retitled this part of the index to reflect costs of urban nursing homes and adult day care. We're not sure if the change from home health services to adult day care represents a change in services or a change in referring to the same services. We will assume that the index still measures changes in home health care.

This particular slice of the consumer price index has been going up much faster than the overall CPI. We suspect there are several reasons for this. First of all there is a nationwide shortage of nurses and the cost of attracting and keeping nurses has gone up considerably. Another reason might be the high cost of liability insurance due to lawsuits. Probably the biggest reason for higher yearly cost increases with nursing homes is the pricing of private pay rates. Although we have no evidence for this assumption, it is fairly common knowledge that nursing homes make up for lack of government reimbursement for their services by charging higher rates for private pay patients. And since government reimbursements have on average been declining, nursing homes have probably been increasing private pay rates at a higher pace than the rate of inflation.

US CONSUMER PRICE INDEX FOR URBAN NURSING |

The data below were derived from Bureau of Labor statistics available online. We need to point out that these data are national averages. Regional rates may vary. You can expect inflation to be higher in urban areas with tight bed supply. But higher inflation rates may also reflect compliance with newly passed, tougher state staffing legislation as well as higher costs from tough state penalty laws and resulting lawsuits. |

|

Here is another look at the changes in nursing home and home health costs compared to changes in the broad consumer price index.

| Broad Consumer Price Index for 1987 to 1997 -- | 3.67% | ||||

| Nursing Home Consumer Price Index for 1987 to 1997 -- | 8.63% | ||||

| Broad Consumer Price Index for 1997 to 2005 -- | 2.69% | ||||

| Nursing Home Consumer Price Index for 1997 to 2005 -- | 5.05% | ||||

Assisted living

The BLS does not measure the cost of assisted living. The annual MetLife survey does report a change in over all prices from the previous year, but this is probably not a reliable indication of inflation. The MetLife survey is not a thorough sample of all assisted living prices and may not reflect the cost of all assisted living services. Since assisted living facilities are generally not reimbursed by the government and since they use few medical services, we should probably assume that year to year increases in cost are going to follow fairly closely the overall CPI rates.

Home health agencies

Traditional home health agencies rely extensively on reimbursement from Medicare. Based on the complaints from agency associations, we must assume that Medicare does not reimburse completely all costs associated with these services. We must assume therefore that private pay patients are paying the difference to provide profits. Home health agencies also rely heavily on medical services such as doctors, nurses, therapists and social workers and this piece of the economy has been increasing in cost much faster than the CPI. Therefore we must assume that home health agency costs are going up faster than general inflation.

Adult day care

Adult day care comes in two forms: nonmedical services and medical services. Starting next year Medicare will probably use medical service adult day care as an alternative to home health care. Using the same assumptions as above, we will have to assume that in the future adult day care costs will rise faster than the general rate of inflation. Non medical service adult day care will probably match the overall inflation rate.

Hospice

As a general rule, the elderly typically don't pay out of pocket for hospice care because Medicare covers this. But if someone were to purchase these services they would probably be going up at a faster rate every year in the general inflation rate. Again, hospice has a heavy medical component and probably suffers from reimbursement problems as do other companies relying on the government.

Personal or non-medical home care

Personal or non-medical home care services do not rely on government reimbursement nor do they use medical services. These are like many service businesses who hire untrained or partially trained employees to provide services. Unless there is a shortage of workers in the future, we will have to assume that yearly increases in the costs of these services will more closely match the overall rate of inflation.

Sample Analysis on the Effect of Different Rates of Inflation

We have provided an analysis below to show how differing rates of inflation for different long-term care services can affect the cost and available amount of future care. In the example below, we make the assumption that our planning for long-term care costs will cover a yearly inflation rate of 5%. We assume that nursing home costs will go up by 5.5% but non-medical home care costs will only increase by 3%. As you can see from the analysis, the further out you go in years, the less you can buy in nursing home services but the more you can buy in a home health-care services.

So how does this affect your planning decisions? Let's suppose you buy a long-term care insurance policy that pays $3,000 a month for nursing home in assisted living costs but only pays $2,000 a month for home health care. If you needed the policy for nursing home tomorrow you would have to come up with an additional $1,500 to cover the sample cost of our nursing home in the analysis. This would have to come from Social Security and possibly some savings. The policy would pay 67% of the cost of the nursing home. But 24 years from now, because nursing home costs have been growing faster than the automatic increase in the policy, you would only have enough to cover 60% of the cost and would have to come up with more out of pocket to cover the difference.

On the other hand, if you needed the policy tomorrow for home care it would give you about 6.3 hours of care per day at the going rate of $16 per hour. But 24 years from now, you could get 9.7 hours per day if the going rate only increased by 3% a year as opposed to the 5% a year your policy benefit is going up. As a general rule we might infer that home health benefits with insurance policies that have a 5% automatic compound benefit increase will buy more hours of care in the future than they will today. In other words for home care, the policy becomes more valuable with age. This knowledge may be helpful to you in planning the future cost and amount of care.

| The Effect of Inflation on Future Benefits | ||||

| Compound Rate of Yearly Benefit Increase | 5.0% | |||

| Initial Monthly Home Care Benefit | $3,600 | |||

| Initial Monthly Nursing Home Benefit | $3,600 | |||

| Average Home Care Hourly Cost | $16.00 | |||

| Average Actual Nursing Home Monthly Cost | $5,000 | |||

| Yearly Increase in Home Care Cost | 3.0% | |||

| Yearly Increase in Nursing Home Cost | 5.5% | |||

| Year | Home Care Benefit | Nursing Home Benefit | Daily Hours of Home Care Benefit Available | Percent of Nursing Home Costs Covered |

| 1 | $3,600 | $3,600 | 7.5 | 72% |

| 2 | $3,780 | $3,780 | 7.6 | 72% |

| 3 | $3,969 | $3,969 | 7.8 | 71% |

| 4 | $4,167 | $4,167 | 7.9 | 71% |

| 5 | $4,376 | $4,376 | 8.1 | 71% |

| 6 | $4,595 | $4,595 | 8.3 | 70% |

| 7 | $4,824 | $4,824 | 8.4 | 70% |

| 8 | $5,066 | $5,066 | 8.6 | 70% |

| 9 | $5,319 | $5,319 | 8.7 | 69% |

| 10 | $5,585 | $5,585 | 8.9 | 69% |

| 11 | $5,864 | $5,864 | 9.1 | 69% |

| 12 | $6,157 | $6,157 | 9.3 | 68% |

| 13 | $6,465 | $6,465 | 9.4 | 68% |

| 14 | $6,788 | $6,788 | 9.6 | 68% |

| 15 | $7,128 | $7,128 | 9.8 | 67% |

| 16 | $7,484 | $7,484 | 10.0 | 67% |

| 17 | $7,858 | $7,858 | 10.2 | 67% |

| 18 | $8,251 | $8,251 | 10.4 | 66% |

| 19 | $8,664 | $8,664 | 10.6 | 66% |

| 20 | $9,097 | $9,097 | 10.8 | 66% |

| 21 | $9,552 | $9,552 | 11.0 | 65% |

| 22 | $10,029 | $10,029 | 11.2 | 65% |

| 23 | $10,531 | $10,531 | 11.5 | 65% |

| 24 | $11,057 | $11,057 | 11.7 | 65% |

| 25 | $11,610 | $11,610 | 11.9 | 64% |

| 26 | $12,191 | $12,191 | 12.1 | 64% |

| 27 | $12,800 | $12,800 | 12.4 | 64% |

| 28 | $13,440 | $13,440 | 12.6 | 63% |

| 29 | $14,112 | $14,112 | 12.9 | 63% |

| 30 | $14,818 | $14,818 | 13.1 | 63% |

| 31 | $15,559 | $15,559 | 13.4 | 62% |

| 32 | $16,337 | $16,337 | 13.6 | 62% |

| 33 | $17,154 | $17,154 | 13.9 | 62% |

| 34 | $18,011 | $18,011 | 14.1 | 62% |

| 35 | $18,912 | $18,912 | 14.4 | 61% |

| 36 | $19,858 | $19,858 | 14.7 | 61% |

| 37 | $20,851 | $20,851 | 15.0 | 61% |

| 38 | $21,893 | $21,893 | 15.3 | 60% |

| 39 | $22,988 | $22,988 | 15.6 | 60% |

| 40 | $24,137 | $24,137 | 15.9 | 60% |

| 41 | $25,344 | $25,344 | 16.2 | 60% |

| 42 | $26,611 | $26,611 | 16.5 | 59% |

| 43 | $27,942 | $27,942 | 16.8 | 59% |

| 44 | $29,339 | $29,339 | 17.1 | 59% |

| 45 | $30,806 | $30,806 | 17.5 | 58% |

Inflation and Long-Term Care Insurance

We have great concern with the inflation protection strategy used by some group long-term care insurance providers. Below is an example taken from actual rates for a group policy offered to employees participating in a state-sponsored health insurance plan.

The strategy is to provide benefits claiming to offer automatic inflation protection but requiring the insureds to purchase additional coverage every three years. When you strip the automatic inflation protection rider out of most long-term care insurance policies, this can cause the premiums to be reduced by half or more. Apparently the providers of this coverage want enrollees to think they're getting more for their money than an equivalent individual policy with built-in inflation protection.

The myth promoted by employers and insurance companies as well as the media is group long-term care insurance is less expensive than individual insurance. This is only true for companies that have high participation rates or if the enrollee has major medical problems. Otherwise group policies are more expensive. We have provided an example below from an equivalent group policy at Notre Dame University , which is the same policy offered by the insurance provider on the left but without automatic inflation protection.

What appear to be very affordable rates for the group plan without inflation turn out to be extremely expensive if the option to purchase additional coverage is exercised every three years. In the example below a couple buys benefits for $800 a year that appear to be identical to benefits from a MetLife policy for $1,678 a year or from the Notre Dame group policy for $2,864 a year.

In fact all benefits are fairly equivalent with the exception of automatic inflation protection. The premiums on the more expensive policies include an automatic increase in benefits of 5% every year. With the cheaper policy additional benefits must be purchased. Here's the scary part. Note that by age 80, the couple will be paying $19,741 a year if they had purchased inflation protection every three years. By that time they will have paid out $141,632 and total premiums. With the Notre Dame policy the couple should still be paying $2,864 a year in premiums and a total of $88,784 in total premiums at age 80. With the MetLife policy the couple should still be paying $1,678 a year and a total of $52,018 by age 80. All three policies would have identical benefits due to inflation protection at that age.

Chart to Help You Estimate The Future Cost of Care

The chart below will help you determine how much money you will need to have in order to fund the future cost of long term care services. Use this table in its static form. Here's how:

The form assumes a current monthly cost of ,000 for long term care. Suppose you want to figure the cost for $3,000 a month. Using your calculator divide $3,000 by $5,000. This gives you .600. Use this number to multiply any number in the body of the chart and it will adjust for $3,000 a month.

The form also assumes that the cost of care increases by 5% per year. This means that 14 years from now the same service costing $5,000 today will cost $10,000. To adjust the chart for a different inflation, divide the inflation you want to use by 5%. As an example, suppose you want to use 4 % inflation. On your calculator divide 4% by 5%. This gives you .800. Use this number to multiply any number in the body of the chart and it will adjust for a 4% inflation rate.

Now let's use the table. Let's first use the current table assumptions of $5,000 a month of costs increasing annually by 5%. Suppose you want to know how much money it will take 20 years from now when you will need care. Go down the column labeled "years" to the number 20. In the columns to the right determine how many years of care you want. For example, 5 years of care 20 years from now would require $758,085.

The amount above was based on ,000 in current costs increasing by 5% per year for 20 years. Use the instructions above to determine different monthly costs and different rates of inflation. For example, our 20 year amount of $758,085 based on a $3,000 a month cost can be determined by dividing $3000 by $5000= .600 and multiplying .600 times $758,085 which yields the new value of $454,851 needed 20 years from now.

To further adjust, for example, for a 4% instead of a 5% inflation rate, divide 4% by 5%= .800 and multiply .800 times $454,851 yielding a new value of $363,881 needed at 20 years.

| DETERMINING THE FUTURE COST OF CARE | |||||||

| Amount of future funds needed to pay $5000 a month in equivalent, current care costs at a 5% annual increase in costs. | |||||||

| Current Monthly Long Term Care Cost | $5,000 | ||||||

| Yearly Increase in Long Term Care Cost | 5.0% | ||||||

| Years | Date | 1 Year's Worth of Future Benefit Costs | 2 Years' Worth of Future Benefit Costs | 3 Years' Worth of Future Benefit Costs | 4 Years' Worth of Future Benefit Costs | 5 Years' Worth of Future Benefit Costs | 6 Years' Worth of Future Benefit Costs |

| 1 | 2005 | $60,000 | $120,000 | $180,000 | $240,000 | $300,000 | $360,000 |

| 2 | 2006 | $63,000 | $126,000 | $189,000 | $252,000 | $315,000 | $378,000 |

| 3 | 2007 | $66,150 | $132,300 | $198,450 | $264,600 | $330,750 | $396,900 |

| 4 | 2008 | $69,458 | $138,915 | $208,373 | $277,830 | $347,288 | $416,745 |

| 5 | 2009 | $72,930 | $145,861 | $218,791 | $291,722 | $364,652 | $437,582 |

| 6 | 2010 | $76,577 | $153,154 | $229,731 | $306,308 | $382,884 | $459,461 |

| 7 | 2011 | $80,406 | $160,811 | $241,217 | $321,623 | $402,029 | $482,434 |

| 8 | 2012 | $84,426 | $168,852 | $253,278 | $337,704 | $422,130 | $506,556 |

| 9 | 2013 | $88,647 | $177,295 | $265,942 | $354,589 | $443,237 | $531,884 |

| 10 | 2014 | $93,080 | $186,159 | $279,239 | $372,319 | $465,398 | $558,478 |

| 11 | 2015 | $97,734 | $195,467 | $293,201 | $390,935 | $488,668 | $586,402 |

| 12 | 2016 | $102,620 | $205,241 | $307,861 | $410,481 | $513,102 | $615,722 |

| 13 | 2017 | $107,751 | $215,503 | $323,254 | $431,006 | $538,757 | $646,508 |

| 14 | 2018 | $113,139 | $226,278 | $339,417 | $452,556 | $565,695 | $678,834 |

| 15 | 2019 | $118,796 | $237,592 | $356,388 | $475,184 | $593,979 | $712,775 |

| 16 | 2020 | $124,736 | $249,471 | $374,207 | $498,943 | $623,678 | $748,414 |

| 17 | 2021 | $130,972 | $261,945 | $392,917 | $523,890 | $654,862 | $785,835 |

| 18 | 2022 | $137,521 | $275,042 | $412,563 | $550,084 | $687,605 | $825,127 |

| 19 | 2023 | $144,397 | $288,794 | $433,191 | $577,589 | $721,986 | $866,383 |

| 20 | 2024 | $151,617 | $303,234 | $454,851 | $606,468 | $758,085 | $909,702 |

| 21 | 2025 | $159,198 | $318,396 | $477,594 | $636,791 | $795,989 | $955,187 |

| 22 | 2026 | $167,158 | $334,316 | $501,473 | $668,631 | $835,789 | $1,002,947 |

| 23 | 2027 | $175,516 | $351,031 | $526,547 | $702,063 | $877,578 | $1,053,094 |

| 24 | 2028 | $184,291 | $368,583 | $552,874 | $737,166 | $921,457 | $1,105,749 |

| 25 | 2029 | $193,506 | $387,012 | $580,518 | $774,024 | $967,530 | $1,161,036 |

| 26 | 2030 | $203,181 | $406,363 | $609,544 | $812,725 | $1,015,906 | $1,219,088 |

| 27 | 2031 | $213,340 | $426,681 | $640,021 | $853,361 | $1,066,702 | $1,280,042 |

| 28 | 2032 | $224,007 | $448,015 | $672,022 | $896,030 | $1,120,037 | $1,344,044 |

| 29 | 2033 | $235,208 | $470,415 | $705,623 | $940,831 | $1,176,039 | $1,411,246 |

| 30 | 2034 | $246,968 | $493,936 | $740,904 | $987,873 | $1,234,841 | $1,481,809 |

| 31 | 2035 | $259,317 | $518,633 | $777,950 | $1,037,266 | $1,296,583 | $1,555,899 |

| 32 | 2036 | $272,282 | $544,565 | $816,847 | $1,089,129 | $1,361,412 | $1,633,694 |

| 33 | 2037 | $285,896 | $571,793 | $857,689 | $1,143,586 | $1,429,482 | $1,715,379 |

| 34 | 2038 | $300,191 | $600,383 | $900,574 | $1,200,765 | $1,500,957 | $1,801,148 |

| 35 | 2039 | $315,201 | $630,402 | $945,603 | $1,260,804 | $1,576,004 | $1,891,205 |

| 36 | 2040 | $330,961 | $661,922 | $992,883 | $1,323,844 | $1,654,805 | $1,985,766 |

| 37 | 2041 | $347,509 | $695,018 | $1,042,527 | $1,390,036 | $1,737,545 | $2,085,054 |

| 38 | 2042 | $364,884 | $729,769 | $1,113,653 | $1,459,538 | $1,824,422 | $2,189,306 |

| 39 | 2043 | $383,129 | $766,257 | $1,153,386 | $1,532,515 | $1,915,643 | $2,298,772 |

| 40 | 2044 | $402,285 | $804,570 | $1,206,855 | $1,609,140 | $2,011,425 | $2,413,710 |

Funding Options

Family Arrangement

This involves a commitment by family to share the cost of long term care and typically involves children taking care of parents. The most common funding is to buy long term care insurance, since this keeps costs low and every participant has a fixed monthly or yearly cost.

Contingency Funding

A contingency fund is money set aside in cash or investments that can easily and quickly be liquidated to pay for long term care. The fund can take two forms: 1) monthly cash payments set aside over a long period or 2) retirement savings that are not spent or that are being hoarded in old age.

As a rule, if a person can't qualify for long term care insurance then setting aside money is the next best alternate. But if insurance is available, then it is much cheaper than a set-aside. Depending on when care is needed, the set-aside can cost anywhere from 5 times to 20,000 times the cost of insurance premiums.

There are problems associated with using unspent retirement savings for long term care:

- As people age, they tend to hoard cash, probably out of fear for the future. They'd rather do without than spend it. The need for long term care paid services isn't going to change that attitude. For example a spouse will often try to cope with care at home without spending money. She usually destroys her physical and emotional health rather than spending money on aides, home care services or respite care. If she doesn't succumb to early death, often the family steps in and spends the money anyway but now it's for care for both of them.

- To throw away money for long term care that required sacrifice in earlier years to put away seems such a waste. If it's not going to be spent during a person's life, why not leave it to the family or a favorite charity where it will do more good. Protect the money with long term care insurance. The interest earnings on $80,000 of money in the bank will easily pay for an insurance policy for a 75 year-old. Using earnings only, leaves the money intact to be used for more worthwhile purposes.

- If for some reason you are forced to spend retirement money for care, this will deplete resources needed by a healthy spouse when the care recipient dies. Invariably, family income drops when one spouse dies. The extra money in savings might be needed for the survivor to maintain enough income to get by and keep the home.

Knowing How Much to Put Away

The chart below will help you determine how much money you have to put away monthly in order to fund the future cost of long term care services. Use the table, here's how.

The form assumes a current monthly cost of $5,000 for long term care. Suppose you want to figure the cost for $3,000 a month. Using your calculator divide $3,000 by $5,000. This gives you .600. Use this number to multiply any number in the body of the chart and it will adjust for $3,000 a month.

The form also assumes that the cost of care increases by 5% per year. This means that 14 years from now the same service costing $5,000 today will cost $10,000. To adjust the chart for a different inflation, divide the inflation you want to use by 5%. As an example, suppose you want to use 4 % inflation. On your calculator divide 4 by 5. This gives you .800. Use this number to multiply any number in the body of the chart and it will adjust for a 4% inflation rate.

Now let's use the table. Lets use the current table assumptions of $5,000 a month of costs increasing annually by 5%. Suppose you want to know how much money to put away every month from now until 20 years from now when you will need care. Go down the column labeled "years" to the number 20. In the columns to the right determine how many years of care you want. For example, 5 years of care 20 years from now would require $758,085. Now go to the shaded columns on the far right and find the corresponding 5 year benefit column. Go down that column to the 20 th year and the amount in the box is the monthly amount you need to set aside for the next 20 years to fund 5 years worth of care. This amount is $1,881.

These assumptions were based on $5,000 in current costs increasing by 5% per year. Use the instructions above to determine different monthly costs and different rates of inflation. For example, our 20 year amount of $758,085 based on a $3,000 a month cost can be determined by dividing $3000 by $5000= .600 and multiplying .600 times $758,085 and also times $1,881 which yields the new values of $454,851 at $1,129 per month set aside to fund $3,000 per month of current cost increasing 5% per year for 20 years.

To further adjust, for example, for a 4% instead of a 5% inflation rate, divide 4% by 5%= .800 and multiply .800 times $454,851 and times $1,129 yielding new values of $363,881 needed at 20 years requiring $903 per month be set aside.

| FUNDING CARE COSTS THROUGH A SAVINGS ACCOUNT | |||||||||

| Monthly payments needed to fund $5000 a month in care costs @ 5% earnings, a 5% annual increase in costs and adjusted for a 20% tax rate. | |||||||||

| Current Monthly Long Term Care Cost | $5,000 | State and Federal Income Tax | 20.0% | ||||||

| Yearly Increase in Long Term Care Cost | 5.0% | Earnings Adjusted for Taxes | 5.0% | ||||||

| Years | Date | 1 Year's Worth of Future Benefit Costs | 2 Years' Worth of Future Benefit Costs | 3 Years' Worth of Future Benefit Costs | 5 Years' Worth of Future Benefit Costs | Monthly Payment for a 1 Year Benefit | Monthly Payment for a 2 Year Benefit | Monthly Payment for a 3 Year Benefit | Monthly Payment for a 5 Year Benefit |

| 1 | 2005 | $60,000 | $120,000 | $180,000 | $300,000 | $4,886 | $9,773 | $14,659 | $24,432 |

| 2 | 2006 | $63,000 | $126,000 | $189,000 | $315,000 | $2,501 | $5,003 | $7,504 | $12,507 |

| 3 | 2007 | $66,150 | $132,300 | $198,450 | $330,750 | $1,707 | $3,414 | $5,121 | $8,535 |

| 4 | 2008 | $69,458 | $138,915 | $208,373 | $347,288 | $1,310 | $2,620 | $3,930 | $6,551 |

| 5 | 2009 | $72,930 | $145,861 | $218,791 | $364,652 | $1,072 | $2,145 | $3,217 | $5,362 |

| 6 | 2010 | $76,577 | $153,154 | $229,731 | $382,884 | $914 | $1,828 | $2,743 | $4,571 |

| 7 | 2011 | $80,406 | $160,811 | $241,217 | $402,029 | $801 | $1,603 | $2,404 | $4,007 |

| 8 | 2012 | $84,426 | $168,852 | $253,278 | $422,130 | $717 | $1,434 | $2,151 | $3,585 |

| 9 | 2013 | $88,647 | $177,295 | $265,942 | $443,237 | $652 | $1,303 | $1,955 | $3,258 |

| 10 | 2014 | $93,080 | $186,159 | $279,239 | $465,398 | 99 | $1,199 | $1,798 | $2,997 |

| 11 | 2015 | $97,734 | $195,467 | $293,201 | $488,668 | $557 | $1,114 | $1,671 | $2,784 |

| 12 | 2016 | $102,620 | $205,241 | $307,861 | $513,102 | $522 | $1,043 | $1,565 | $2,608 |

| 13 | 2017 | $107,751 | $215,503 | $323,254 | $538,757 | $492 | $984 | $1,475 | $2,459 |

| 14 | 2018 | $113,139 | $226,278 | $339,417 | $565,695 | $466 | $933 | $1,399 | $2,332 |

| 15 | 2019 | $118,796 | $237,592 | $356,388 | $593,979 | $444 | $889 | $1,333 | $2,222 |

| 16 | 2020 | $124,736 | $249,471 | $374,207 | $623,678 | $425 | $851 | $1,276 | $2,127 |

| 17 | 2021 | $130,972 | $261,945 | $392,917 | $654,862 | $409 | $817 | $1,226 | $2,043 |

| 18 | 2022 | $137,521 | $275,042 | $412,563 | $687,605 | $394 | $788 | $1,181 | $1,969 |

| 19 | 2023 | $144,397 | $288,794 | $433,191 | $721,986 | $381 | $761 | $1,142 | $1,903 |

| 20 | 2024 | $151,617 | $303,234 | $454,851 | $758,085 | $369 | $738 | $1,107 | $1,844 |

| 21 | 2025 | $159,198 | $318,396 | $477,594 | $795,989 | $358 | $717 | $1,075 | $1,791 |

| 22 | 2026 | $167,158 | $334,316 | $501,473 | $835,789 | $349 | $697 | $1,046 | $1,744 |

| 23 | 2027 | $175,516 | $351,031 | $526,547 | $877,578 | $340 | $680 | $1,020 | $1,700 |

| 24 | 2028 | $184,291 | $368,583 | $552,874 | $921,457 | $332 | $664 | $996 | $1,661 |

| 25 | 2029 | $193,506 | $387,012 | $580,518 | $967,530 | $325 | $650 | $975 | $1,625 |

| 26 | 2030 | $203,181 | $406,363 | $609,544 | $1,015,906 | $318 | $637 | $955 | $1,592 |

| 27 | 2031 | $213,340 | $426,681 | $640,021 | $1,066,702 | $312 | $625 | $937 | $1,561 |

| 28 | 2032 | $224,007 | $448,015 | $672,022 | $1,120,037 | $307 | $613 | $920 | $1,533 |

| 29 | 2033 | $235,208 | $470,415 | $705,623 | $1,176,039 | $302 | $603 | $905 | $1,508 |

| 30 | 2034 | $246,968 | $493,936 | $740,904 | $1,234,841 | $297 | $593 | $890 | $1,484 |

| 31 | 2035 | $259,317 | $518,633 | $777,950 | $1,296,583 | $292 | $585 | $877 | $1,462 |

| 32 | 2036 | $272,282 | 44,565 | $816,847 | $1,361,412 | $288 | $576 | $865 | $1,441 |

| 33 | 2037 | $285,896 | $571,793 | $857,689 | $1,429,482 | $284 | $569 | $853 | $1,422 |

| 34 | 2038 | $300,191 | $600,383 | $900,574 | $1,500,957 | $281 | $562 | $842 | $1,404 |

| 35 | 2039 | $315,201 | $630,402 | $945,603 | $1,576,004 | $277 | $555 | $832 | $1,387 |

| 36 | 2040 | $330,961 | $661,922 | $992,883 | $1,654,805 | $274 | $549 | $823 | $1,372 |

| 37 | 2041 | $347,509 | $695,018 | $1,042,527 | $1,737,545 | $271 | $543 | $814 | $1,357 |

| 38 | 2042 | $364,884 | $729,769 | $1,130,653 | $1,824,422 | $269 | $537 | $806 | $1,343 |

| 39 | 2043 | $383,129 | $766,257 | $1,153,386 | $1,915,643 | $266 | $532 | $798 | $1,330 |

| 40 | 2044 | $402,285 | $804,570 | $1,206,855 | $2,011,425 | $264 | $527 | $791 | $1,318 |

Sale of Assets

Tangible assets that might produce enough income to pay for long term care might include investment property such as rentals, commercially leased property, land, a farm, second home or a business.

Some individuals are heavy into real estate and short on cash. If the intent was to cash out of the investment at some future point, then a sale is warranted. But as with the contingency fund, it seems a shame to sacrifice in early years to establish an investment only to throw it away to long term care. It would make more sense to use income from the investments to buy long term care insurance and save the investments for something more worthwhile.

Long term Care Insurance-- Why Should You Buy It?

- It will help you keep your independence and dignity. Here's how. . . some of you will spend all your assets on care while others plan to give their money away or put it in trust. With no assets you will now qualify for a welfare program called Medicaid. Medicaid typically pays for a semiprivate room in a nursing home, and; not all nursing homes take Medicaid patients. In many states it's not easy to get Medicaid to cover home care or pay for assisted living. Many people want to stay at home, but with Medicaid may not be able to. And assisted living is rapidly becoming a preferred alternative to nursing home care for certain disabilities but Medicaid may insist on a nursing home instead.

- If you are married and you have a need for long term care, your spouse may be forced to pay for an outside caregiver. The cost is likely to come from your combined income and assets. If the need for paid care drags on too long, your spouse may be left with minimal cash assets for future needs. Insurance solves this problem and allows your spouse to keep the assets.

- Many healthy care-giving spouses won't spend their money and choose to "tough it out" on their own without help. If care of a disabled spouse drags on too long, this can have a devastating effect on the physical and emotion health of the caregiver.

- Surveys reveal that healthy caregivers often don't spend their money for help but they will use insurance if available. Insurance allows the healthy caregiver to buy much-needed respite from paid professionals, while at the same time, retaining the assets and possibly avoiding an early death from the mental and physical stress of care giving.

- If your children or extended family promise to take care of you if the time comes that you need care, insurance will help them do that. Probably neither you nor your children have thought of the prospects of moving you from place to place, changing your dirty diapers, cleaning up after "accidents" in the bathroom or helping you with bathing and dressing. Insurance will pay for aides to help with these tasks.

- If you are single and a need for long term care arises, insurance can pay for and coordinate that care. With insurance you won't have to feel you would be a burden for family or friends.

- If you have the desire to leave assets behind when you die, insurance will help preserve those assets from the cost of long term care.

How to Buy Long term Care insurance

There are hundreds of long term care insurance companies selling hundreds of different types of policies. It can become very confusing. There are various conditions for home care and nursing home care, waiting periods, qualifying periods, inflation clauses and the list goes on. Here is a checklist of some of the things you need to know before you purchase a policy.

LONG TERM CARE INSURANCE BUYING CHECKLIST

the more "yes" answers you get the better off you are

- Is the insurance company rated at least A, A+ or A++ by A.M. Best?

- Is it a large diversified company selling more than just long-term care insurance?

- Is the insurance representative an expert in long-term care insurance? (Because of its complexity, almost all LTCi experts only sell LTCi; they seldom sell anything else.)

- Is the insurance representative an independent representing at least 5 or more companies? (Captive agents or agents for large life insurance companies are limited to only one policy to offer.)

- Does the representative have a degree and/or industry financial designations?

- Does the representative own a personal long-term care insurance policy?

- Is the policy you like tax qualified and if not, do you understand the ramifications?

- Are there at least 6 ADL's allowed for certification?

- Does it allow "standby assistance"?

- Is it a "pool of money" as opposed to a "stated period"?

- Is it "integrated" as opposed to "2-pool"? (2-pool is not allowed in some states and these policies are becoming very rare.)

- Do you understand how the elimination period works? (This is extremely important.)

- Does it have an absence of prohibitive cost containment provisions?

- Is there an absence of "capping" of automatic benefit increase riders?

- Do you understand how the waiver of premium works?

- Does the assisted living facility benefit pay the same as for nursing home?

- Are you buying adequate home care coverage?

- Does the company have a history of rate increases?

- Does the policy pay for homemaker services?

- Does the policy offer an alternative plan of care for coverage that doesn't exist today?

You Should Buy Long Term Care Insurance When You Are Younger

There is a bonus to buying long term care insurance at a younger age. The premium is lower. The chart below illustrates this point. A person currently age 45 buying a typical policy with a spouse would spend $30,884 in total premiums to age 78.

Suppose the person above chose to wait to buy the equivalent coverage at age 65. If that same policy were available when the same person were 65--highly unlikely since carriers change policies about every 2 years--and purchased then, he would pay $55,411 in total premiums over his 13 remaining years to age 78.

With either scenario, the person would own the same benefit coverage at his age 78 but would pay about 2 1/2 times more in premiums by waiting 20 years to purchase.

This scenario doesn't even address the additional problem that by waiting to buy, a person's health may become poor and he or she might lose the 10% to 20% good health discount. Or even worse, by waiting to buy, a person may become uninsurable.

Long Term Care Insurance Cost

Comparison--Buying Now vs. Waiting

| $3,000 per Month Benefit | |||||

| $180,000 Total Benefit | |||||

| Comprehensive | |||||

| 100% Home Care | |||||

| 90 Day Elimination | |||||

| 5% per Year Automatic Benefit Increase | |||||

| (Couple, age 45 buy today or wait 10 years or wait 20 years) | |||||

| Age 45-buys $3,000 per month; amount automatically increases 5% per year | |||||

| Age 55-buys equivalent amount of $4,887 (4,900) per month due to 5% yearly increase | |||||

| Age 65-buys equivalent of $7,960 (8,000) per month due to 5% yearly increase | |||||

| Policy Owner Age 45 Applies With Spouse Age 45 (Or Delay Buying) | |||||

| Age | Total Cost | Total Cost | Monthly Benefit | Total Benefit | Cost per Dollar |

| Monthly | to Age 78 | at Age 78 | at Age 78 | of Benefit | |

| 45 | $67.73 | $30,884 | $15,001 | $900,574 | $0.03 |

| 55 | $125.93 | $34,759 | $15,001 | $900,574 | $0.04 |

| 65 | $355.20 | $55,411 | $15,001 | $900,574 | $0.06 |

| Current Cost For Selected Ages (Couple Apply, Same Age For Both) | |||||

| Age | Total Cost | Total Cost | Monthly Benefit | Total Benefit | Cost per Dollar |

| Monthly | to Age 78 | at Age 78 | at Age 78 | of Benefit | |

| 45 | $67.73 | $30,884 | $15,001 | $900,574 | $0.03 |

| 55 | $76.31 | $21,062 | $9,215 | $552,874 | $0.04 |

| 65 | $134.04 | $20,910 | $5,657 | $339,417 | $0.06 |

Reverse Mortgage

A reverse mortgage is a special type of loan used by older Americans to convert the equity in their homes into cash. The money obtained through a reverse mortgage can provide seniors with the financial security they need to fully enjoy their retirement years.

The reverse mortgage is aptly named because the payment stream is reversed. Instead of the borrower making monthly payments to a lender, as with a regular first mortgage or home equity loan, a lender makes payments to the borrower. While a reverse mortgage loan is outstanding, the borrower owns the home and holds title to it and does not make any monthly mortgage payments.

The money from a reverse mortgage can be used for ANYTHING: daily living expenses; home repairs and home improvements; medical bills and prescription drugs; payoff of existing debts; education; travel; Long term health care; prevention of foreclosure; and other needs. If your home needs physical repairs (mandatory repairs) in order to qualify for a reverse mortgage, a portion of the proceeds will be set aside for this purpose.

You can choose how to receive the money from a reverse mortgage. The options are: all at once (lump sum); fixed monthly payments (for up to life); a line of credit; or a combination of a line of credit and monthly payments. The most popular option B chosen by more than 60 percent of borrowers B is the line of credit, which allows you to draw on the loan proceeds at any time.

The size of the reverse mortgage that you can get will depend on your age at the time you apply for the loan, the type of reverse mortgage you choose, the value of your home, current interest rates, and B sometimes B where you live. In general, the older you are and the more valuable your home (and the less you owe on your home), the larger the reverse mortgage can be.

The costs associated with getting a reverse mortgage include the origination fee (which can usually be financed as part of the mortgage), an appraisal fee, and other charges similar to those for regular mortgages. The money provided to you from a reverse mortgage is tax-free; it is not income that you must pay taxes on. However, the funds received from a reverse mortgage may affect your eligibility for certain kinds of government assistance, so you should check into this before getting a reverse mortgage.

Before applying for a reverse mortgage, you must first meet with a reverse mortgage counselor. You may, however, first approach a reverse mortgage lender, who can provide you with the names of approved counseling agencies in your area. A list of approved counseling agencies nationwide is posted on the Web by the US Department of Housing and Urban Development. The counselor = s job is to educate you about reverse mortgages, to inform you about other alternative options available to you given your situation, and to assist you in determining which particular reverse mortgage product would best fit your needs if you elect to get a reverse mortgage. In general, counseling sessions must be done face-to-face. However, if you are seeking a Fannie Mae reverse mortgage you can do it by telephone. In some areas, telephone counseling may be available for consumers seeking an FHA reverse mortgage (Home Equity Conversion Mortgage).

No payments are due on a reverse mortgage while it is outstanding. The loan becomes due and payable when the borrower ceases to occupy their home as their principal residence. This can occur if the senior (the last remaining spouse, in cases of couples) passes away, sells the home, or permanently moves out of the home. The home does not have to be sold to pay off the loan. The borrower (or their borrower's heirs) can instead pay off the reverse mortgage and keep the home. In any event, the amount owed on the reverse mortgage cannot exceed the value of the home at the time that the loan must be repaid. Moreover, if the home is sold and the sale proceeds exceed the amount owed on the reverse mortgage, the excess proceeds go to the borrower or the borrower = s estate.

As with any other mortgage, you hold the title and the bank holds a lien against the property. There are no income or credit requirements for reverse mortgages. Virtually anyone over age 62, with a home that qualifies can get the loan. And there are no risks with the popular HECM loan. It's fully insured by FHA. The bank can't demand any more money from you or your family if it turns out there isn't enough equity to repay the loan.

Reverse mortgages generally don't produce enough money to pay for extended long term care. A small loan, however, can produce enough in premium payments to leverage a large long term care insurance benefit.

Getting Money Out of Life Insurance Without Dying

Some Common Strategies

- Borrow against the cash value of the life insurance policy.

- Instruct the life insurance carrier to cash out the policy, based on the available cash surrender value.

- Determine if the life insurance carrier offers an "accelerated benefits program" rider and if the insured is eligible.

- Sell the life insurance policy in a viatical or life settlement.

- Borrow from friends or family using the life insurance policy as collateral to secure the loan.

- A combination of an "accelerated benefit" and a viatical settlement may be possible and might net more cash than either by itself!

Viatical Settlements

Individuals have been selling or trading their ownership of life insurance policies since the very beginning of the insurance industry. This, however, was a relatively unknown practice until the AIDS epidemic heightened in the late 1980's. As policyholders stricken with the disease learned that there was a living value to life insurance, the Viatical Settlement Industry was born.

After a decade of industry growth, legislation, and regulation, viaticals have become an important financial option to many terminally-ill individuals. By selling a policy, many of these policyholders can ease the financial burdens brought on by increased medical costs and compensate for their loss of income due to illness.

Benefits to Insured's / Policy Owners

- Immediate Cash to Ease Financial Burdens

- Additional Money to Compensate for Loss of Income

- Relief of Monthly Premium Expenses

- Funds to Seek Treatments Not Covered by Health Insurance

- Funds to Pay off Debts Now, Instead of Burdening Family Members in the Future

- Settlement Income May Be TAX-FREE!!!

Viatical Settlement Qualifications

- Only non-contestable life insurance policies are considered.

- Insurance Company must be rated B+ or better.

- Minimum face value of $50,000 - NO MAXIMUM. Lower face values are considered if multiple policies total over $50,000.

- All types of policies qualify, including term, whole life, universal life, joint-survivorship, group, corporate-owned policies (COLI), key-man, and life policies held in irrevocable life insurance trusts.

- Policy Owner may be the insured, a company, a family member, a charity or any other entity with an insurable interest in the life of the insured.

Insured's Health Status:

• Terminally-ill individuals with limited life expectancies of 5 years or less are considered.

• Terminal illnesses may include cancers, heart disease, AIDS, Alzheimer's disease, ALS, or any other life threatening disease.

• Copies of medical records are obtained for verification of health status. No medical exams are required!